Allan McHale, Director of Memoori, reviews the business case for convergence and integration in buildings, and explains why this will change business models and have a significant impact on mergers, acquisitions and alliances. This is part one of a two-part contribution.

Allan McHale, Director of Memoori, reviews the business case for convergence and integration in buildings, and explains why this will change business models and have a significant impact on mergers, acquisitions and alliances. This is part one of a two-part contribution.

This is a complex subject because it involves so many different stakeholders in the supply chain, with some being protective of the status quo and seeing integration as a possible threat. The technology is not well understood by all and is not bound by common standards, and it requires collaboration among organizations that have never had to work together. This article examines a set of tools to explain the linkages between building control infrastructures and communications and IT, and then evaluates the benefits in order to establish if customers' value propositions are met. Three case studies from different vertical markets are then reviewed. Part two to be published next month will focus on the security industry aiming to deliver total solutions and explain the need to change business models through partnerships, impacting mergers, acquisitions and alliances on the supply side.

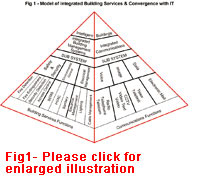

In the mid 1980s, building controls started to go digital. For safety reasons, there was a need to transfer information from different technical infrastructures, and digital systems were more cost-effective. To understand the complexities, the author developed a model in 1989 (see Fig 1). The left-hand face shows the individual building services, progressively moving up to integrate subsystems that provided more comprehensive control. The right-hand face contains the communication functions and similarly brings these together. At the top of the pyramid, both integrated systems can be linked together to create an intelligent building.

Over time, the various stages of integration on the left came about, starting with stage one where the functions were hardwire-linked. Stage two integrated  subsystems through a serial link connected to a common supervisory computer. Stage three connected systems on a higher level LAN that allowed information to be delivered to any PC on the system. Stage four was peer-to-peer connection across all the different control systems, possibly using a common communication protocol.

subsystems through a serial link connected to a common supervisory computer. Stage three connected systems on a higher level LAN that allowed information to be delivered to any PC on the system. Stage four was peer-to-peer connection across all the different control systems, possibly using a common communication protocol.

Most large buildings constructed in the last five to 10 years were integrated at stage three, and this was the first sign that using TCP/IP over Ethernet would play a major role in bringing about integration with the right-hand face that had been using this technology. It was not until 2005 when, through advancements in digital technology and adoption of XML and Web services, eureka — a holistic solution — was realized. One could now satisfy the value propositions of building owners and operators by delivering improved performance and operation of the building and enterprises within.

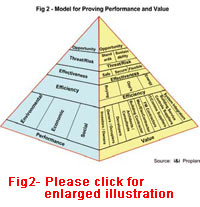

Progress over the last 20 years has been slow, despite technical improvements; there was little coordination among the many different stakeholders. Therefore, in 2004, the model was extended (see Fig 2) to show the other two sides of the pyramid, performance and value, in order to develop a tool to investigate the benefits of integration and intelligence in buildings. The base of the performance face is made up of three prime drivers: economic, social and environmental. Economic issues include cost (both first-time and lifecycle), adaptability/ flexibility, increased productivity and operating cost. The economic drivers may carry more weight than social and environmental ones, but certainly not in all instances. Environmental factors include meeting future legislative needs (for example, the European Energy Performance in Buildings Directive, or EPBD), building regulations, government incentives and tax schemes. On the social scale, there is increasing pressure on corporate bodies to include green issues as just one part of their social responsibilities, along with providing the right air quality, temperature, and safety and security for their employees. These can have a direct impact on improving productivity in the workplace, and are vital in some environments like hospitals.

At the next level of analysis, four other sieves are introduced that will evaluate the benefits to be unlocked from integration, information and intelligence in buildings.  These are Efficiency, Effectiveness, Threat/Risk and Opportunity, and these can be measured across the full spectrum of demand drivers. For example, a hospital owner/operator could unlock economic, environmental and social benefits by using a patient communication system to operate local lighting and temperature control while delivering other services such as nurse calls and entertainment. This could reduce first-time cost, improve productivity, reduce energy cost and reduce a patient's time spent in a hospital. It is technically feasible, and one of the case studies mentioned shows how this has been achieved.

These are Efficiency, Effectiveness, Threat/Risk and Opportunity, and these can be measured across the full spectrum of demand drivers. For example, a hospital owner/operator could unlock economic, environmental and social benefits by using a patient communication system to operate local lighting and temperature control while delivering other services such as nurse calls and entertainment. This could reduce first-time cost, improve productivity, reduce energy cost and reduce a patient's time spent in a hospital. It is technically feasible, and one of the case studies mentioned shows how this has been achieved.

If one now looks at the value face of the pyramid, one must ask "value to whom." Although it is quite clear that without it being of value to the owner/end user integration will not take place, if it is not also of benefit to other parties in the supply chain, then they are likely to put up barriers.

The base of the value face is made up of 10 different stakeholders involved in the building supply chain. Integration will, at the very least, mean change for all in the supply chain, and this for some could derail them from their present power base. For others, new opportunities will result from integration. In all cases, it is possible to evaluate through qualitative measures but much more difficult to quantify. The suggested criteria to measure are efficiency, effectiveness and threat/risk; these will decide profit and opportunity, which are shown at the pinnacle of the pyramid.

In 2006, a test on IT convergence in buildings was carried out in the United States. The report shows that proving performance and value was vital for users to change their buying habits and adopt the new integration. To convert pragmatists, one has to prove performance and value of IT convergence through real-life cases and demonstrate the ROI(details at: ebbasedbuildingtechnologies.blogspot.com). Though three years old, these case studies are still relevant because they are based on real numbers.

ROI is key in convincing building owners, and most are looking for a quick return. Most of the respondents from the real-estate business were looking for a return of no more than three years. However, the ROI can be influenced by other factors than reducing operating costs, such as increasing rental value, reducing vacancy rates and adding new revenue streams. These drivers can be significant, depending on whether the building is rented out or occupied by the owner, and whether the tenant or building owner is responsible for maintaining and paying for utilities.

Thus, the differentiators that will have impact on the relative importance of demand drivers will vary, dependent on ownership, type of building, complexity and process, and whether it is a new construct, major refurbishment or retrofit. The case studies identified clearly illustrate the importance that these different factors have had on influencing the investment decision for installing converged systems. It should be mentioned that they have all been delivered through partnerships.

The digital hospital in Omaha, Nebraska delivers to its patients a much more effective level of care while reducing medical and operational costs. This is a good example of how connecting the technical infrastructures to the business  enterprise has brought about true synergy. The health care business across the developed world is now undergoing some fundamental changes to meet changes in patient demographics, advances in drugs and medical treatments, and provide a holistic social model of health-gain. This requires the adoption of patientcentered approaches to the delivery of health care; despite the considerable inertia to change, the challenge is being taken up. Good building design, based on patientcentered requirements, is gradually being adopted, and this has brought about the need to integrate building technical services, or further, to interface with patient administration and medical care services. Other building types that have benefited in a similar way are airports, science and high-tech buildings, educational establishments, and retail and hotel chains.

enterprise has brought about true synergy. The health care business across the developed world is now undergoing some fundamental changes to meet changes in patient demographics, advances in drugs and medical treatments, and provide a holistic social model of health-gain. This requires the adoption of patientcentered approaches to the delivery of health care; despite the considerable inertia to change, the challenge is being taken up. Good building design, based on patientcentered requirements, is gradually being adopted, and this has brought about the need to integrate building technical services, or further, to interface with patient administration and medical care services. Other building types that have benefited in a similar way are airports, science and high-tech buildings, educational establishments, and retail and hotel chains.

The move toward an IT-centric approach and the role that XML and TCP/IP are playing in convergence and integration in intelligent buildings will have a major impact on the way business is conducted in the future. What makes convergence important is that XML is incorporated in IT Infrastructures both within major companies and across the Web. IT infrastructures will eventually carry all the information that management will analyze and act upon to both improve building and estate performance and provide holistic solutions that will also affect the operations being carried out in the building. Building owners will seek out suppliers to partner with them to ensure that they get robust and reliable solutions that are cost-effective and appropriate for their needs. Understanding and making the business case will be key to winning business in this new environment where more business will be conducted directly with the client, instead of the traditional contractual procedures.

For this market to really expand, it requires the backing and commitment from large companies that have the technical and financial muscle to inspire customers to adopt robust solutions that will add value and performance to their buildings. These players will come from IT, network/communication, technical infrastructure and infrastructure integration backgrounds.