INSIGHTS

Security in 2010 saw a rebound in activity. Allan McHale, Director of Memoori, delves into key M&A trends and considers what could happen in 2011. This is Part 2 of a two-part series; Part 1 was in our February issue.

STRATEGIC DRIVERS

In the last two years, M&A activity has been driven by strategic buys, particularly by the major global security companies, defense companies and from outside the security business — IT and communication companies and more recently validation, authentication and biometric companies. This dynamic seems to continue to apply in 2011 and beyond.

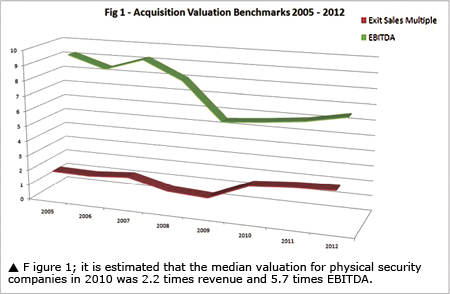

Security Business:M&A Drivers,Valuation and Investment

Date: 2011/05/05

Source: Submitted by Memoori Business Intelligence

In 2009, we recorded 17 announcements of capital injection by venture capital companies, with total funds amounting to US$144 million. In 2010, the total investment was $142 million from 19 arrangements. The majority of these involved investment in US companies by US venture capitalists. However, in 2010, there was a flurry of activity in renegotiating debt financing, particularly by established companies, and the consensus was that the industry is now in a much stronger financial state.

Few venture capital companies specialize in the physical security industry, and it is clearly not the most attractive technology sector. However, there are segments within in it that are particularly attractive to them: information security, identity and security solutions, and defense. The former is regarded as having massive potential.

IDENTIFY M&A TARGETS

One of the major sources for M&As is the continual flow of start-ups. The security industry has produced a very rich seam of new companies that are developing cutting-edge products particularly associated with IP-based video surveillance. The epicenter of entrepreneurship in the physical security industry is currently firmly established in the IP video business. The U.S. is home to approximately 37 percent of these companies, and the next most populated country is the U.K. at 13 percent, followed by Korea at 11 percent, Taiwan at 7 percent, Germany at 6 percent, and China, Japan and Israel at 4 percent.

In the U.S., almost half of these companies were founded around 2000. This is an astonishingly high percentage of new companies, and it is not evidenced in any other country that we have reviewed. So, the U.S. has not just spawned more companies, but they are much younger. None of the other countries in our sample had established new start-ups younger than four years, and only Israel, Taiwan, Germany and the U.K. had more than 12 percent of companies younger than 10 years old.

The U.S. leads in entrepreneurship in this field because the technology to produce the new digital video solutions comes from the electronics and IT industries where the U.S. already leads. The second reason is that all the support needed for setting up new ventures is well-established both in terms of financial investment and management skills. Both of these are well-practiced and encouraged in the U.S., particularly in Silicon Valley and Boston areas; we estimate that approximately 50 percent of the new companies in this business are clustered in these 2 regions. Finally, American culture encourages risk taking; failure does not necessarily have stigma attached to it that it does in Europe